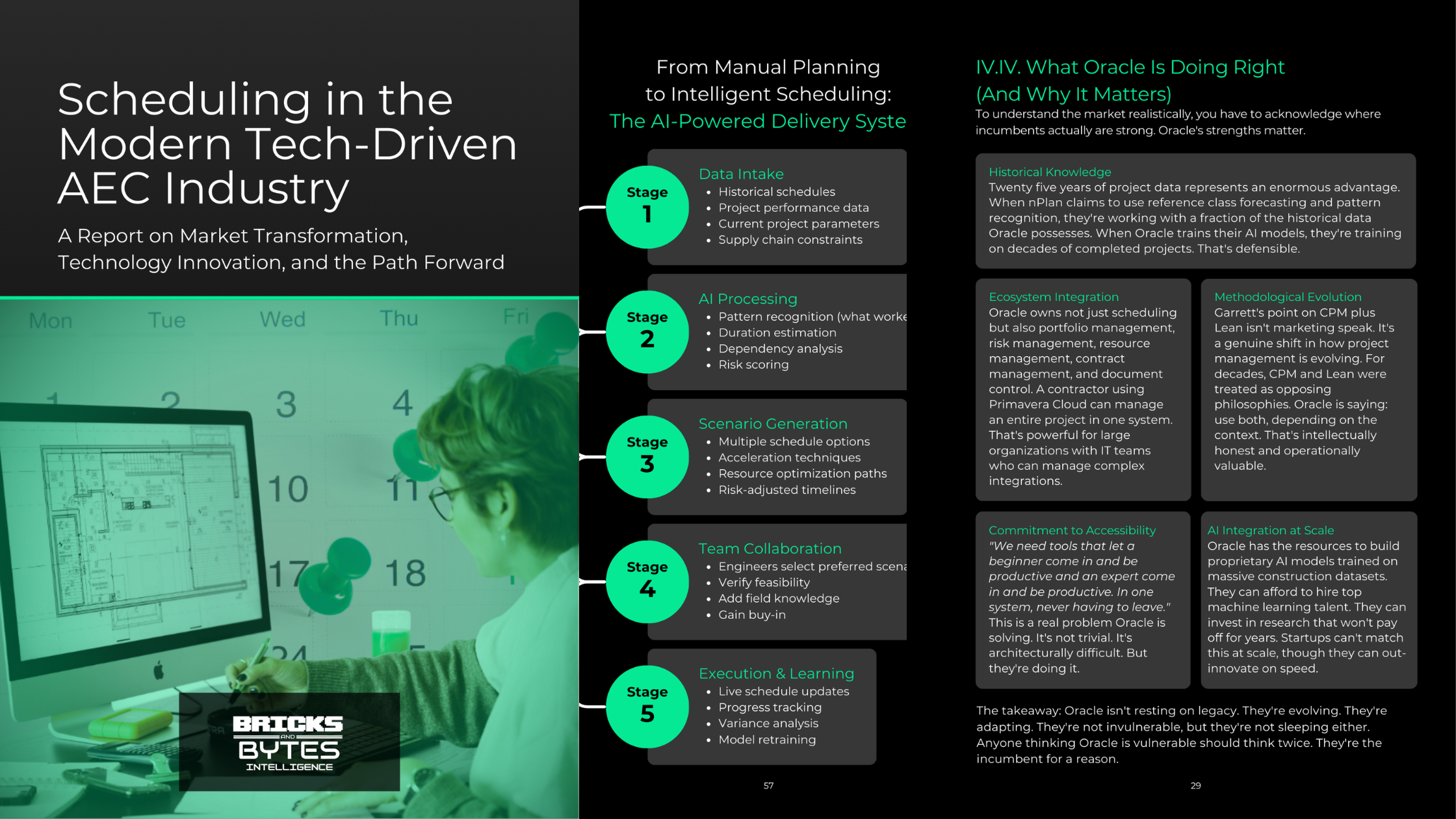

INDUSTRY INSIGHTSThe One Thing PE Looks For When Buying AEC Companies A software vendor proves their innovation works on a project. Results are clear. ROI is measurable. But when they try to scale across the organization, momentum dies. This isn’t a product problem. It’s structural. Darren Martin spent years as Chief Digital Officer at Atkins Realis, where he led enterprise digital transformation across a 40,000-person global organization. More recently, he transitioned to advising private equity firms on AEC acquisitions and now serves as Chief Investment & Technology Officer at AInvested, a firm focused on purposeful innovation investment and transformational strategy. He sees a pattern repeatedly: the vendors with the best technology aren’t necessarily the ones that scale. The ones that scale are those that understand why organizational bottlenecks exist in the first place. The pilot works. The organization doesn’t. Credit: Getty Images TL;DR: Your pilot works. Enterprise adoption stalls because AEC is structurally fragmented, not because your product is weak. Project managers own project P&L, not transformation. They lack mandate and incentive to scale innovation. Features don’t scale. Outcomes do. Boards care about margin, schedule, safety, and labor efficiency. PE buys transformation potential, not current revenue. Valuation = the gap between today and a digitally transformed future. Mid-tier AEC exits are accelerating due to consolidation and baby-boomer sell-offs. PE doesn’t replace teams. It backs them to execute. Perform, and you stay. Fail, and leadership changes. Bottom line: Scaling in AEC is an organizational and GTM problem. Tie your tech to board-level outcomes, or it won’t scale. Your Innovation Works. So Why Doesn’t It Scale? Projects succeed. Pilots prove value. And then enterprise adoption stalls. The reason isn’t technical. It’s organizational, and it runs deeper than most founders realize. Project managers are fighting daily fires: labor shortages, supply chain disruptions, weather impacts, and pricing constraints from original bids. These managers are accountable for their project’s P&L, not enterprise transformation. They have neither the mandate from above nor the discretion in their contracts to allocate resources to scale innovation across the organization. “Projects can be at pilot subscale forever because they’re passionate projects, and people know that they should have worked, and they don’t quite know why they haven’t worked,” Darren observes. It’s a pattern he’s seen across multiple organizations, and it reveals something important about how AEC is structured differently from other industries. In manufacturing or retail, centralized decision-making authority can force scaling. Here, it can’t. Project managers operate in silos, each protecting their own economics. Even when a technology demonstrably works, the person incentivized to scale it doesn’t have the authority or resources to do so. This bottleneck is unique to AEC, and understanding it is critical for founders trying to scale software and AEC leaders trying to implement innovation. The real question becomes: if the problem is organizational, how do you get past it? The answer lies in who you’re actually selling to. Project leaders are incentivised to protect project P&L, not enterprise change. Credit: BigRentz You’re Selling Features. Decision-Makers Want Outcomes. Tech teams love your product. They see the value immediately. The problem is that tech teams don’t control budget decisions. Decision-makers at the board, C-suite, and CFO level think differently. They care about safety, schedule reduction, margin improvement, and labor efficiency. Not features. Not ease of use. When a vendor presents a workflow demo, decision-makers are asking themselves something entirely different: how much faster can we build, what’s the margin impact, and can we serve more clients with the same headcount? “If someone implements a technology that will reduce rework and improve the schedule by 10%, that’s not the same conversation as ‘what’s my functionality and what’s my price point.’ The second conversation doesn’t drive enterprise adoption,” Darren explains. Most vendors spend months perfecting the first conversation. They talk about workflows, dashboards, and integration. Decision-makers want outcomes. Your GTM strategy is broken until you tie product value to board-level outcomes, not user workflows. Understanding how PE thinks about valuation makes this clear. PE Doesn’t Buy Your Current Revenue. It Buys Your Transformation Potential. When private equity evaluates an AEC acquisition, they ask one fundamental question: What would this company be worth if we digitally transformed it? The acquisition price isn’t based on current revenue. It’s based on the gap between the current state and the transformed state. Consider the math. Current state: $100 million revenue with a traditional labor-intensive model. Transformed state: the same revenue plus 30 percent margin improvement through technology, plus the ability to scale without proportional headcount growth. That gap equals the valuation multiple PE is willing to pay. “We recently bought a company at $1 billion and got involved in valuing that company from a digital transformation perspective,” Darren reflects. “What would it mean to transform the organization? What would be the value if it were transformed?” This matters because if you’re considering an exit, your valuation depends on PE’s belief in a digital transformation story. If you’re acquired, you’re measured on whether you deliver that transformation. But Darren also sees a deeper issue: many companies have sunk investments in digital initiatives that didn’t work. PE will want to understand what failed and why, and whether the next bet will succeed. That’s where the diligence gets rigorous. Capital doesn’t run the business. People do. Credit: Autodesk Why Mid-Tier Exits Are Happening Now Baby boomer ownership is exiting. Proprietary firms, not publicly traded ones, are being acquired at accelerating rates. Consolidation is happening at the mid-tier level through geographic roll-ups, service-line carve-outs, and portfolio builds. What’s driving it: Infrastructure investment is forecast to grow to $13.9 trillion by 2035. PE sees predictable cash flows. Market leaders see geographic expansion opportunity. Timing matters. Who’s acquiring: Market leaders including AECOM, Jacobs, ARUP, and Atkins Realis have been consolidating through acquisitions. Private equity is also active in this space, building portfolios of mid-tier firms rather than pursuing the largest global players, as demonstrated by the trend of baby boomer exits creating acquisition opportunities. If you’re a